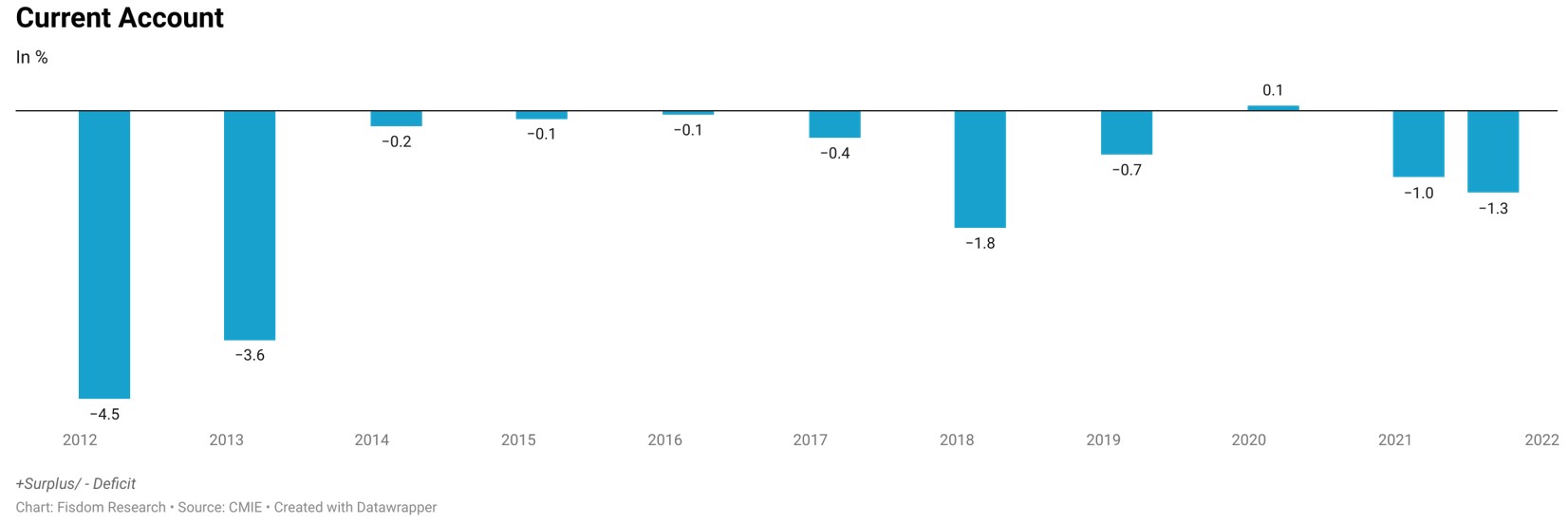

India’s current account situation is strengthening; not out of the woods yet

The current account retrogressed to a deficit of 1.3% of GDP in Q2FY22 as against a surplus of 0.9% of GDP in Q1FY22, dilating trade deficit and a higher drag from net investment income.

The services surplus remained steady. Despite a more comprehensive CAD, the BoP surplus remained robust at USD31.2bn, partly due to a one-time SDR allocation (USD17.9bn) by IMF, which, if excluded, would lower the rest to USD13.3bn. The primary balance (CAD+FDI), which reflects stable current account funding, turned mildly negative amid low FDI.

New global/domestic headwinds amid Omicron and persistent supply constraints are the key factors to watch out for.

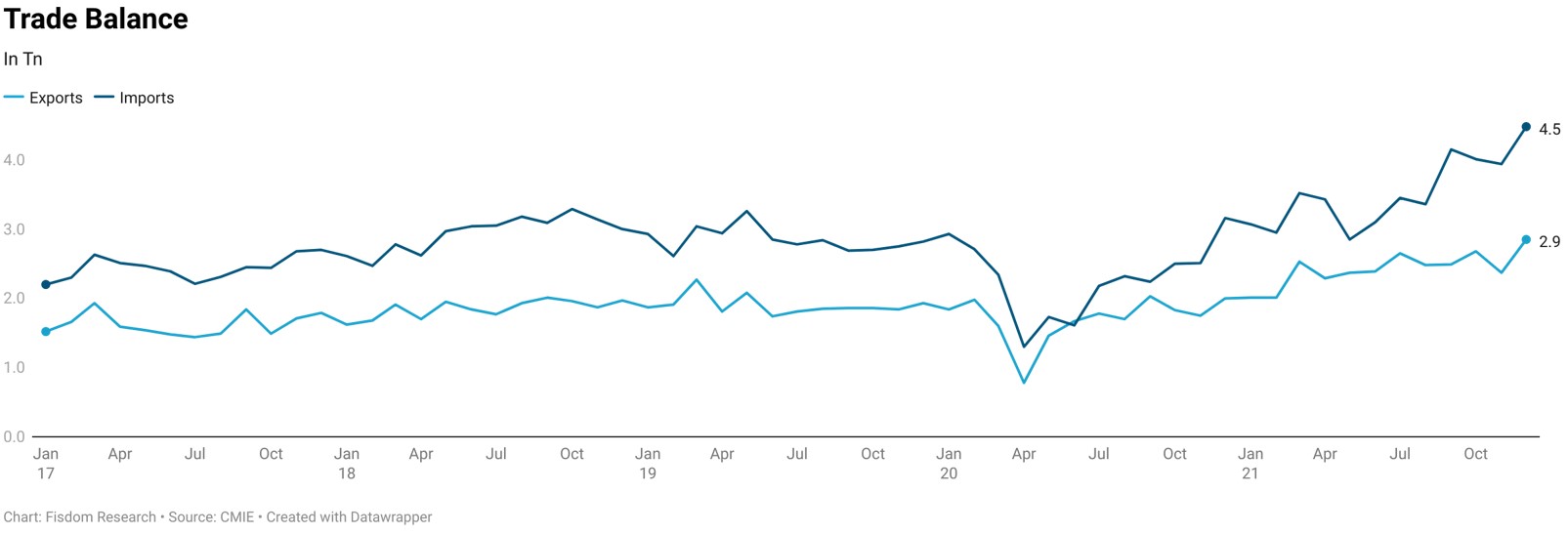

India’s trade deficit at record high as exports weakens; currency depreciation could extend support

December was the fourth straight month of elevated trade deficit (1.63 trillion), close to the earlier high of 1.67 trillion recorded in September’21. Imports of crude oil petroleum products, non crude oil & petroleum products & even gold silver imports went up by 11%, 15% & 12% respectively.

We think higher commodity prices and a relatively more robust exchange rate could play into the widening deficit more than the demand. Falling domestic currency could extend support to the weakening exports. However, implications of the Omicron variant of coronavirus on global trade flows and slowing demand from significant export partners pose downside risks to Indian exports.

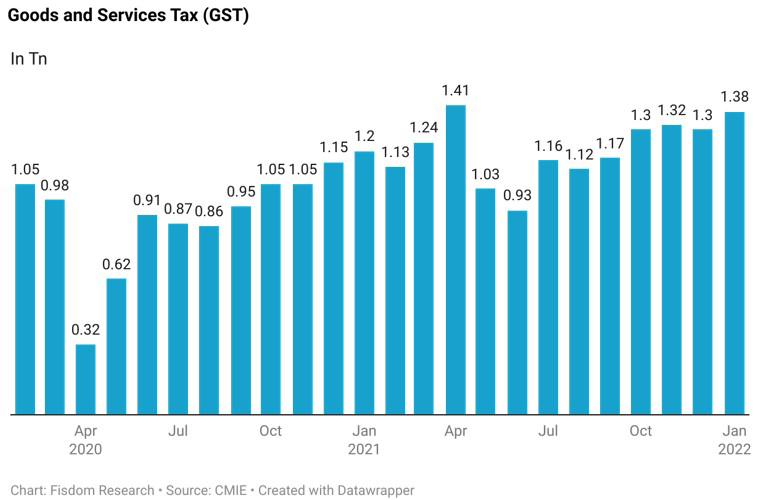

GST collections second highest since inception & e-way bill fell 4% m-o-m

GST collections for January 2022 went up by 15% YoY to INR. 1.38 Tn. It is the second-highest collection since the implementation of GST.

Coupled with economic recovery, anti-evasion activities, especially action against fake billers, have improved GST. The improvement in revenue has also been due to various rate rationalization measures undertaken by the Council to correct the inverted duty structure. The positive trend in the revenues will continue in the coming months.

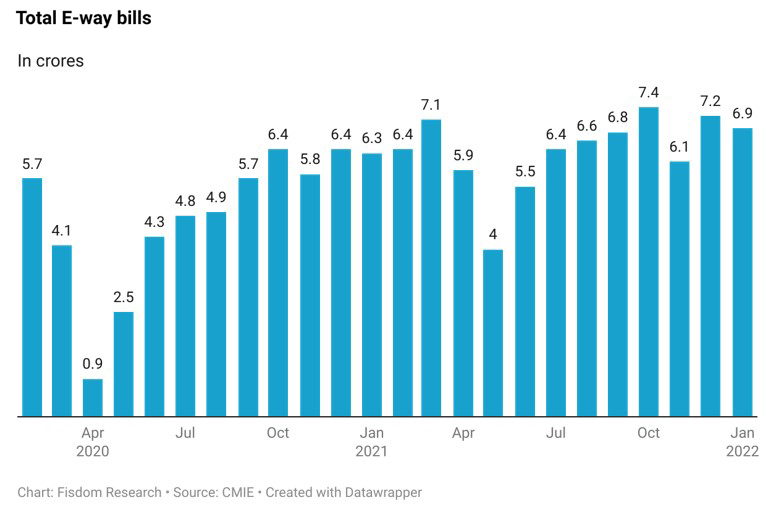

E-way bill generation touched fell by 4% MoM but was up by 12.4% compared with Nov’21. Some stretch in trade due to the spread of the Omicron variant affected the e-way bill generation.

In the latest budget, even the government projected an average GST collection of INR.1.3 lakh crore a month for FY23 compared to an average of INR.1.13 lakh crore assumed for FY22. It might well achieve it. There are reports that the technical glitches in the GST backbone have been fixed, leading to better compliance and coupled with sustained momentum in the economy should do the trick.

Download the full report to get the complete coverage